You can get a loan with a County Court Judgment (CCJ) on your file while having no guarantor. While many high-street banks will automatically decline your application, alternative business finance lenders assess the situation first. Specialist lenders and commercial finance brokers assess factors like current trading performance, cash flow, and affordability.

This guide explains how CCJ loans with no guarantor work, what alternative lenders consider, and how to improve your application for a successful approval.

What Is a CCJ and Why Does It Affect Borrowing?

A County Court Judgment (CCJ) is a court order registered against an individual or business that has failed to repay a debt. It stays on your credit record for six years from the date of the judgment, regardless of whether you pay it off. If you settle the balance within one month, the CCJ is removed entirely. Pay it after that window but before the six years expire, and it gets marked as “satisfied”, but is still visible to lenders.

For traditional banks, a CCJ is often an automatic red flag. Their lending criteria tend to be rigid and algorithm-driven, which means a single adverse marker can trigger an outright decline before a human even reviews your case. As a result, businesses with otherwise strong trading performance may still fall outside standard bank credit criteria.

The important thing to understand is that a CCJ tells a lender that something went wrong in the past. It does not necessarily tell them anything about how your business is performing right now.

How CCJ Loans Work Without a Guarantor

These funding options have approval processes based on the strength of the business itself rather than the personal creditworthiness of a third party. There are several routes this can take:

Unsecured business loans: Some alternative lenders offer unsecured lending to businesses with CCJs, provided the business can show consistent revenue, up-to-date management accounts, and a clear explanation of the adverse credit. Interest rates will be higher than mainstream products, but the trade-off is access to capital when other doors are closed.

Invoice finance: If your business invoices other businesses, invoice finance allows you to release cash tied up in unpaid invoices. Because the lending is secured against the value of the invoices themselves, your personal or business credit history carries less weight in the assessment.

Asset finance: Similarly, asset-based lending uses existing equipment, vehicles, or machinery as security. Because the lender has a tangible asset to fall back on, they can often approve applications that would be declined on an unsecured basis. Funding Bay offers several asset finance options, including hire purchase, asset refinance, and sale and leaseback arrangements.

Merchant cash advances: For businesses that take card payments, a merchant cash advance provides an upfront sum repaid as a percentage of future card transactions. There is no fixed monthly repayment, and because the lending is tied to revenue, lenders are often more flexible on credit history.

Secured business loans: Where a business can offer property or other high-value assets as collateral, secured lending opens up larger amounts at lower rates. Because the loan is backed by tangible security, lenders typically do not need to scrutinise personal or business credit as rigorously as they would for unsecured facilities.

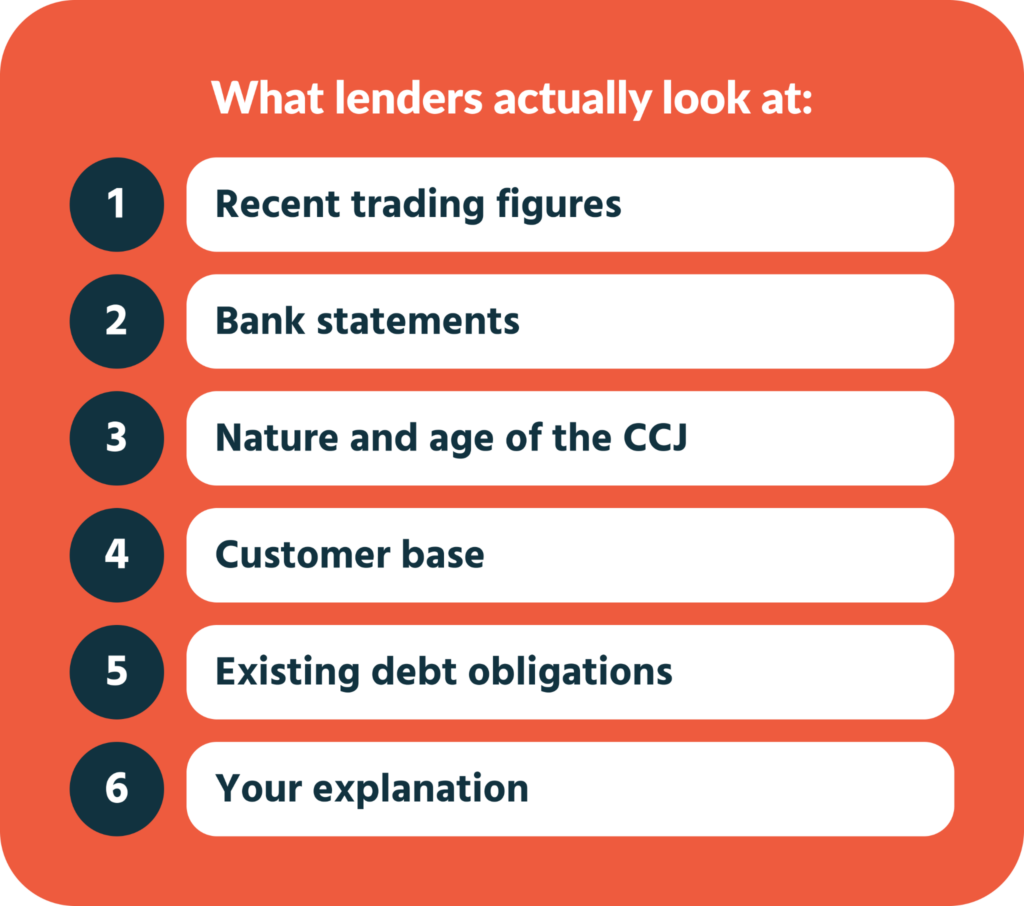

What Lenders Actually Look At

If your credit history includes a CCJ, alternative lenders and specialist loan providers for CCJs will focus on a different set of factors when assessing your application. These typically include your most recent trading figures and management accounts, your bank statements from the last six to twelve months, the nature and age of the CCJ itself (satisfied or outstanding, how long ago it was registered), the strength and diversity of your customer base, any existing debt obligations in the business, and whether you have a clear explanation for what happened and what has changed since.

This is where working with a broker makes a significant difference. Our team at Funding Bay analyses each business’s funding requirements and goals, matches them against the criteria of the lender network, and packages the application accordingly. The application processes are nuanced, and we are experts in making a business’s numbers, narrative, and requirements fit into lender deal boxes.

How to Strengthen Your Application

Start by getting your paperwork in order, your last filed accounts, twelve months of bank statements, and up-to-date management accounts, including a balance sheet and profit and loss statement. If the CCJ has been satisfied, make sure your credit report reflects this accurately. Prepare a brief, honest explanation of the circumstances that led to the judgment and what you have done to address the underlying issue. The stronger your current trading position, the less weight the CCJ carries.

Next Steps

A CCJ does not have to be the end of your borrowing options. The alternative finance market functions to support businesses that are trading well but carry adverse credit markers that put them outside mainstream lending criteria. If your bank has said no, that is one lender’s decision based on one set of criteria. It is not a verdict on your business.